The $10,000 Bill and the End of Large-Denomination American Currency

The 10000 dollar bill still sounds extreme. That is one reason collectors keep returning to it. The note feels unusual even before you know its history. Yet the real story is not just the size of the number. The note makes sense only inside an older banking system, an older transfer culture, and an older view of how money moved across the country.

A coin checker can identify famous numismatic objects quickly, but that is not enough here. The $10,000 bill is not interesting because it is easy to label. It is interesting because it belonged to a category of currency that once had a practical role and later lost that role almost completely. To understand the note, you need to look at the function first, then the history, then the collector’s interest.

Quick Overview of the $10,000 Bill

The $10,000 bill was a high-denomination U.S. note issued for public circulation. It featured Salmon P. Chase on the face. The note was not made for ordinary daily spending. Its role was tied to large-value transfers. In modern collecting, it is known as one of the strongest symbols of America’s large-note era.

Feature

Basic point

Denomination

$10,000

Portrait

Salmon P. Chase

Main role

Large-value transfers

Everyday use

Extremely limited

Collector appeal

Rarity, history, prestige

That short outline explains why the note is famous. It does not explain why it existed. For that, the broader system matters more than the portrait or the face value.

Why The United States Issued Very Large Notes

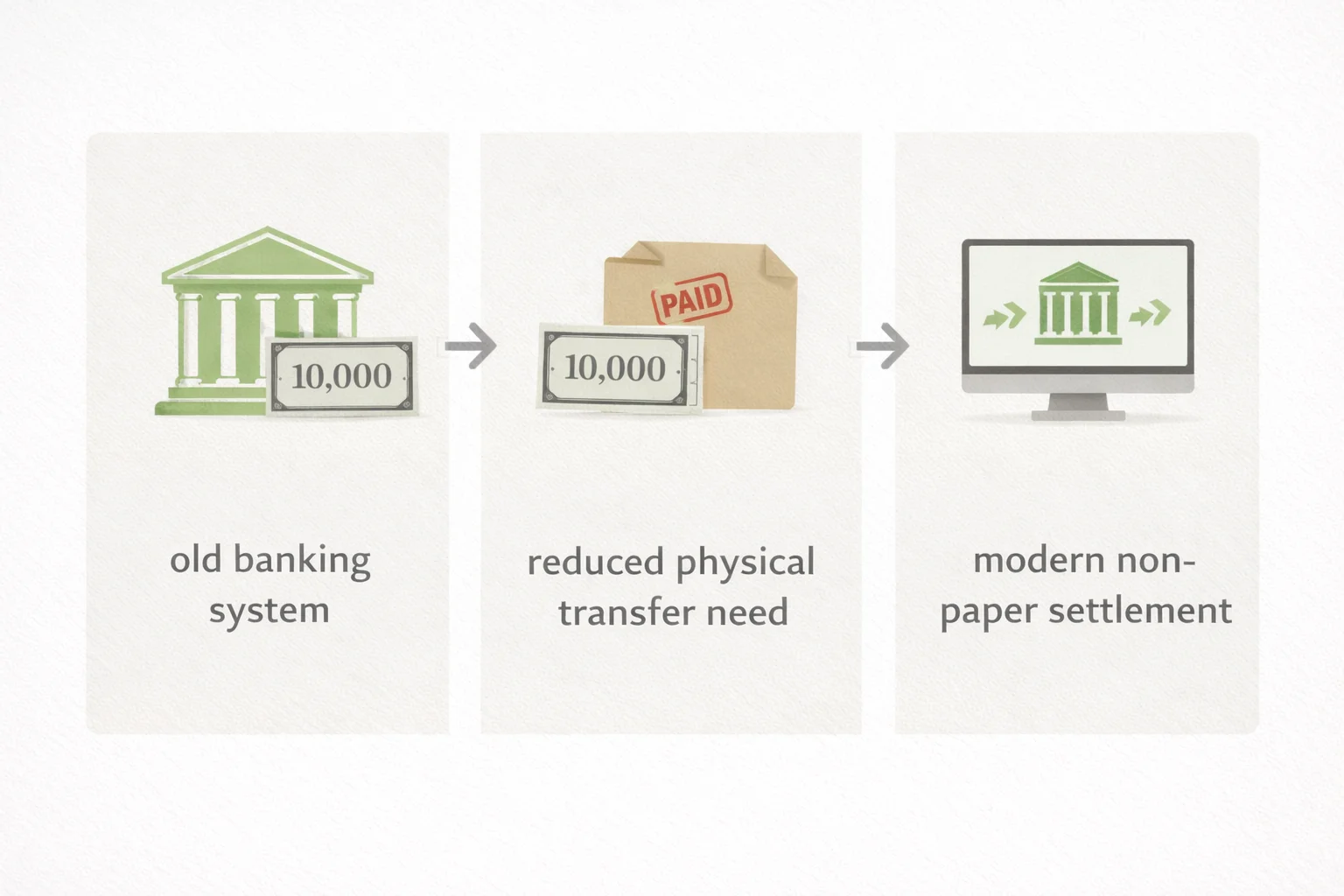

Large-denomination paper money was not created to impress the public. It was created because the financial system once needed compact paper forms for very large transfers. Before digital settlement, wire-based automation, and real-time accounting systems, large sums often moved through banks and institutions in slower and more physical ways.

A very large note solved a simple problem. It reduced the bulk of high-value paper transfers.

The logic was practical:

Large transfers needed compact paper forms

Banking systems worked differently

Electronic settlement has not yet replaced paper movement

Institutions used these notes more than ordinary consumers

This point matters because it corrects a common misunderstanding. The $10,000 bill was never a normal pocket note. It was part of a system built for scale, not for daily shopping.

Where the $10,000 Bill Fits in the Large-Denomination Family

The $10,000 bill was part of a larger group of high-denomination U.S. notes. That group also included the $500, $1,000, and $5,000 bills. These notes were issued for practical reasons. They made large transfers easier and reduced the amount of paper needed for high-value transactions.

Denomination

General collector image

$500

Better known and more discussed

$1,000

Strong collector recognition

$5,000

Much scarcer and more specialized

$10,000

Iconic top-tier public denomination

This hierarchy shaped later collector interest. The lower large denominations are already important. The $10,000 bill sits above them in symbolic power. It became the note that people mention first when they want an example of extreme American paper money.

That fame has a side effect. It makes the note seem more mythic than functional. In reality, it was both. It was a real instrument in a real system, and later it became a trophy object for collectors and historians.

A Short Historical Path

The history of the $10,000 bill does not need a long timeline to make sense. It follows a clear path.

First, large-denomination notes were useful. They matched the needs of banks, Treasury operations, and other high-value institutional activity. Then the financial system changed. Transfer methods improved. The same amount of value is no longer needed to move through such large physical notes. As that change continued, the reason for keeping these notes active became weaker.

The story moves through four simple stages:

Practical issue

Institutional use

Shrinking necessity

Eventual discontinuation

That progression is what turns the note from a banking tool into a historical object.

Why Large-Denomination Currency Lost Its Purpose

The end of the $10,000 bill was not dramatic in the way many people imagine. It was more structural than theatrical. The note did not disappear because it failed as a design. It disappeared because the system around it stopped needing it.

Three changes mattered most.

Banking Changed

Interbank settlement no longer depended on moving huge amounts of paper in the same way. As banking became more efficient, high-denomination notes became less useful. The institution did not need the paper once the process changed.

Public Use Stayed Small

Ordinary consumers did not build daily life around notes like this. The public role was weak from the start. That made discontinuation easier. When a denomination has little normal retail use, the argument for keeping it active becomes thin.

Policy Followed Practicality

Once the need fell, policy followed the logic of the system. The note no longer solves a modern problem. It became easier to retire than to justify.

This is the real end-of-era story. The $10,000 bill did not become obsolete because it was strange. It became obsolete because the financial structure around it evolved.

The End in 1969

Collectors often focus on 1969 because that year marks the formal end of active circulation for these large denominations. That matters, but it should be read carefully. Discontinuation did not mean that every surviving note vanished at once. It meant the government ended its circulation role and removed them from normal monetary life.

That distinction matters for collectors. A discontinued note can still survive. It can still be owned. It can still trade privately. What changes is its function. It stops being practical currency and becomes historical currency.

That shift is exactly what happened here. The $10,000 bill crossed from a financial tool into a collectible object.

Why the $10,000 Bill Still Fascinates Collectors

The note attracts attention for obvious reasons. The face value is huge. The survival pool is small. The market is narrow. Still, collector interest runs deeper than shock value.

What keeps the note important:

Historic role

Very high face value

Limited surviving examples

Museum-level appeal

Strong specialist interest

A note like this carries several layers at once. It is rare paper money. It is a symbol of a past monetary structure. It is also a cultural object. Even people outside numismatics recognize the denomination. That broader recognition adds to its pull.

There is also a prestige factor. Some notes are collected because they fill a slot. The $10,000 bill is collected because it represents a boundary. It marks the upper edge of what public U.S. paper money once looked like.

What Collectors Usually Want to Know First

In a practical sense, collectors usually begin with a few simple questions. These questions do not copy the first article’s note-reading logic. They belong more to history, market position, and category.

A collector usually wants to know:

Which issue is being discussed

How often does it appear publicly

Whether it belongs to a very narrow market

What role did it play before discontinuation

How it fits into the larger-denomination sequence

These are not minor points. They shape the way the note is approached. A $10,000 bill is not treated like an ordinary collectible note with a bigger number. It sits in a different mental category from the start.

Myths Around the $10,000 Bill

Famous notes collect myths very easily. The $10,000 bill is a good example.

Common myths include:

It was a normal pocket note

Face value explains collector value

Discontinued means fully gone

All examples belong only to museums

Every surviving note has the same market position

Each of these ideas oversimplifies the note.

It was not a normal daily-use bill. It was not priced by face value alone once it entered the collector world. Discontinuation did not erase every surviving example. Museums matter, but private collectors matter too. And not every surviving note sits at the same level of rarity or market importance.

This is why collector articles should not stop at the denomination. The moment the article becomes only “look how large this bill was,” the useful part disappears.

What the End of Large-Denomination Currency Tells Us About U.S. Money History

The disappearance of the $10,000 bill says something larger than the fate of one denomination. It shows that money history is tied to systems, not just to designs. A note can be well-made, historically important, and still become unnecessary because the network around it has changed.

That is the bigger lesson.

The end of large-denomination currency reflects:

Changes in banking infrastructure

Less need for physical high-value transfer

A stronger role for non-paper settlement methods

A shift from practical use to historical memory

This is one reason the $10,000 bill remains such a strong teaching object. It explains not just what Americans printed, but why they stopped printing it.

FAQs About the $10,000 Bill

Was the $10,000 bill meant for everyday spending?

No. It was issued for very large transfers and institutional use. Ordinary daily spending was never its main role.

Why did the United States stop using such large notes?

Because the banking system changed. High-value paper movement became less necessary as more efficient transfer methods developed.

Is the $10,000 bill still legal tender?

Yes, in legal-tender status, but no as an active circulating denomination. It is a historical note, not a working modern instrument.

Did all of these notes disappear after discontinuation?

No. Some survived in private hands, institutional holdings, and the specialist market.

Conclusion

The $10,000 bill is not just a famous old note. It is a marker for the end of a monetary system that once relied on very large paper denominations. Its importance comes from function, not only from face value. That is why it still matters to collectors.

Its story also shows where quick numismatic shortcuts stop helping. Even a free coin value app cannot explain why this denomination existed, why it vanished, or why it still carries so much collector weight. Coin ID Scanner, with its AI assistant, can be useful when someone wants a fast numismatic reference habit on the coin side. The $10,000 bill still demands the slower route: history first, category second, collector meaning last.